Playboy, Inc. (Nasdaq: PLBY) is undergoing a transformation to an asset-light business model centered around its iconic brand, positioning the company for sustainable profitability. This may not be a company that screens due to past misadventures in D2C and China licensing which have contributed to its current low market value and dilution, but it now presents significant potential opportunity for investors as management course corrects. The company sold Yandy.com and the Lovers stores chain in 2023 and has recently licensed its digital operations to the world’s biggest adult business that isn’t named Only Fans – Byborg. Now, the benefits of these key strategic structural initiatives are starting to flow through to the financials – Playboy delivered its first quarter of positive adjusted EBITDA in Q1 2025 in over a year. If management can continue to execute, including signing new licensing deals, this is a stock that can easily double.

Shifting to an Asset-Light Business Model

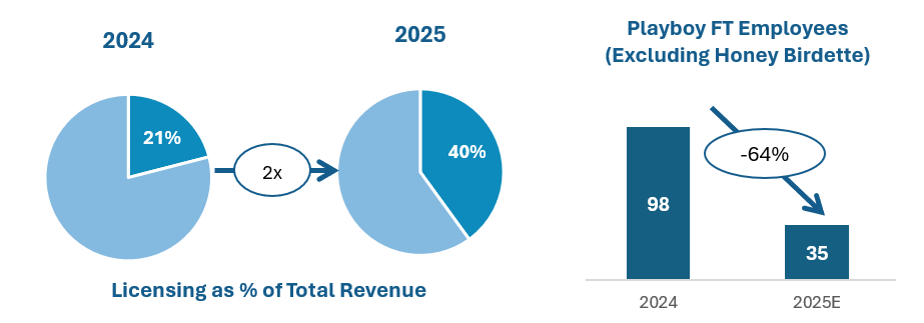

Playboy is transforming itself into an asset-light company focused on generating high-margin licensing revenue from a brand that is internationally renowned. In fact, few brands are as instantly recognizable around the world as Playboy, thanks to its iconic bunny ears and legendary lifestyle image. Already, the mix of licensing revenue is expected to double from 21% in 2024 to 40% in 2025. Far fewer employees are needed to manage a licensing business; Playboy expects the number of full-time employees (excluding Honey Birdette) to decline from 98 in 2024 to 35 in 2025. With lower operating expenses, profitability should be significantly higher.

The asset-light model allows the Playboy to focus on its core strengths – the brand and IP monetization – not operating. The Company retains control over its brand while significantly reducing overhead costs and capital requirements.

Licensing Partnerships to Accelerate Path to Profitability

Licensing is now the central focus area for Playboy. Under a licensing model, the company permits third parties to use its trademarks in exchange for royalties, typically with guaranteed minimum payments. In 2024, the company generated $24.6 million in revenue from the licensing segment, representing 21% of total revenue. The majority of license agreements are long-term in nature (1 to 15 years in length), ensuring visibility of high margin revenue. As of 2024, the licensing contracts included future royalty guarantee payments of approximately $67.4 million through 2034, ensuring a baseline cash flow.

The licensing agreement with premium adult streaming operator Byborg was a massive win for Playboy and its shareholders, delivering a minimum of $300 million in guaranteed payments over the initial 15-year term. As part of the deal, which became effective January 1, 2025, Playboy is licensing its Playboy Club, Playboy Plus, and Playboy TV businesses to Byborg. The deal generated $5 million in revenues during Q1 2025 and is expected to deliver $20 million for the full year 2025. This deal will improve Playboy’s profitability (and liquidity), as evident by positive adj. EBITDA during Q1 2025.

Historically, China has accounted for the majority of Playboy’s licensing revenue. However, the contribution declined as the company terminated several license agreements in China due to non-payment and breaches of contract. To reinvigorate the China business, Playboy entered into a joint venture with CT Licensing Limited, a brand management unit of Fung Group. This JV aims to reinvigorate apparel sales and re‑sign license agreements. The company expects licensing activity to increase in China in 2025, and as such, we expect a multiple new licensing deals to be signed in the near future.

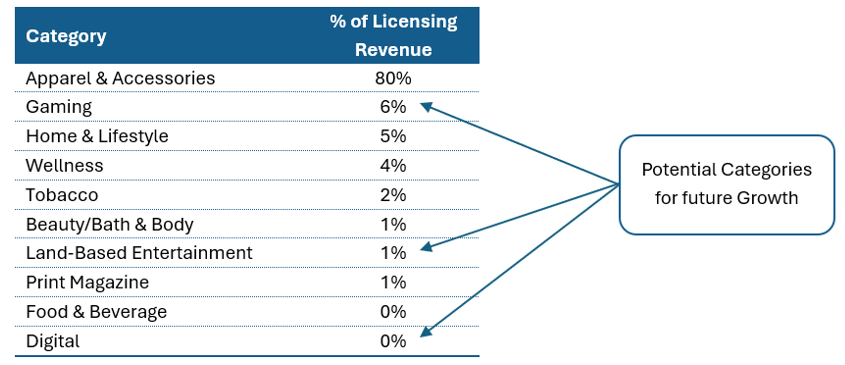

In addition to digital, there is a large opportunity to expand licensing beyond apparel & accessories (~80% of total licensing revenue) into verticals such as gaming and land-based entertainment. Playboy noted that it is actively pursuing new licensing opportunities, particularly in live events and gaming where it has been successful in the past. For example, a Playboy-branded membership club in the United States. Given the brand’s cultural relevance and appeal across demographics, particularly among younger, digitally savvy consumers, we expect to see the bunny in many more places over the coming years. Moreover, Playboy has significant opportunity to further expand its global licensing reach. Currently, the U.S. and China account for 75% of the total licensing revenue. Given Playboy’s strong international brand recognition, there is plenty of room for growth in underpenetrated markets such as Latin America, Southeast Asia, and the Middle East.

Honey Birdette – Showing Improving Profitability

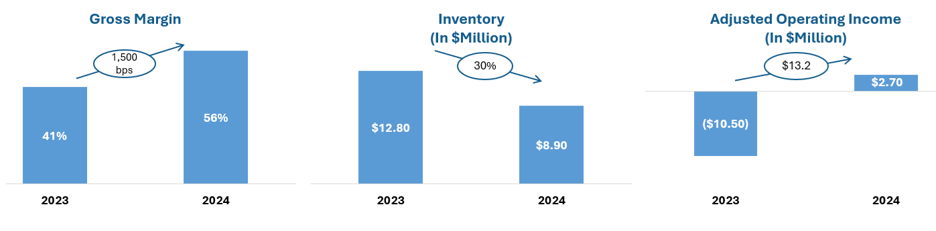

At this point the company’s direct-to-consumer business consists solely of Honey Birdette, a lingerie brand which operates online and via 51 stores in Australia, the United States and the United Kingdom. Honey Birdette accounted for 60% of total revenue as of FY 2024. Playboy acquired Honey Birdette in 2020 for $333 million. It briefly considered selling the brand last year but decided to retain it following the Byborg deal which has given the company breathing room to focus on improving Honey Birdette’s operating metrics and future growth prospects. During 2024, Playboy focused on improving the profitability and cash flow of Honey Birdette. This included reducing inventory levels, days on sale, and closing underperforming stores. This resulted in a 1,500 bps jump in gross margins to 56% and adjusted operating income turned positive in FY 2024. The rebound has continued in Q1 2025 as well, with gross margins further expanding to 58%.

New Revenue Opportunities

Playboy is leveraging its global brand appeal to pursue new revenue opportunities. This includes the relaunch of Playboy magazine in February 2025, which was met with great success, with both online and newsstand copies selling out. The Company plans to release a second issue this year, followed by four issues in 2026. While the magazine itself may not generate significant revenue, there are many adjacent revenue opportunities associated with a strong brand and the magazine’s content including paid voting, events, special editions, calendars, and new content series.

Recent Quarterly Results

Playboy reported solid Q1 2025 results on the back of its transition to an asset-light model, and is a telling indicator of financial performance turning positive. Licensing revenue jumped 175% YOY to $11.4 million, driven by $5.0 million minimum guaranteed royalties received from Byborg. Excluding royalties from Byborg, licensing revenue was up 56% YOY, led by the robust performance of Chinese licensing partnerships signed last year. Direct-to-consumer revenue, comprising the Honey Birdette brand, was $16.3 million, down 13% YOY.

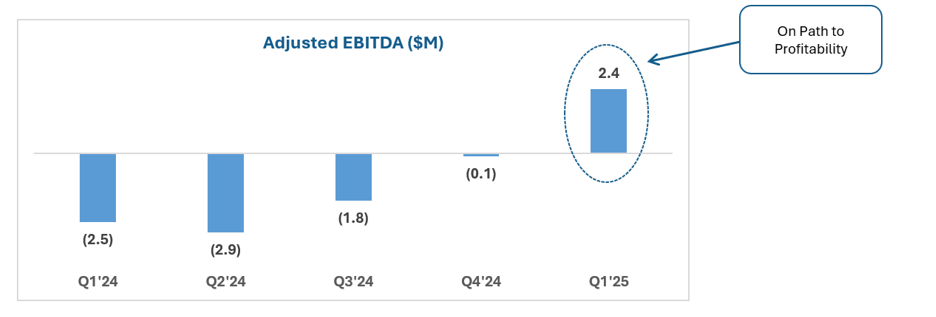

Adjusted EBITDA was $2.4 million, compared to a loss of $2.5 million in Q1 2024. The improvement in profitability was due to royalties received from Byborg and a reduction in operating expenses. Playboy expects revenue for FY 2025 to be $120 million and is guiding to end the fiscal year with positive cash flow.

The total cash & cash equivalents as of the end of Q1 2025 were $25.7 million and long-term debt stood at $155.1 million. While it is unclear if Playboy will continue to be able to reduce net debt to around $100 million by the end of 2025 since shareholders rejected the second tranche of investment from Byborg, we think the company has ample liquidity and has a history of being creative when it comes to the capital markets.

Valuation: Potential for Re-rating

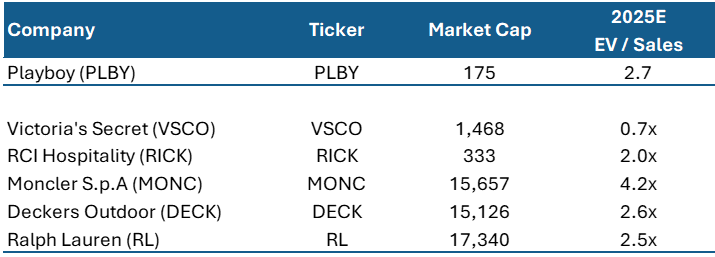

The market is currently valuing PLBY at an enterprise value of approximately $325 million, 2.7x EV/Sales (2025 revenue guidance is $120 million). This does not fully reflect the company’s transition to a high-margin, asset light model, and certainly does not pass the smell test for what someone would pay for one of the world’s most recognizable brands. As the mix shifts towards high-margin licensing business and the profitably re-emerges, we expect PLBY to re-rate to the upper end or even above the 2.0x-4.2x sales multiple range typical of global brand licensors. With the D2C and China licensing headwinds going away, lower overhead costs and reallocation of capital to licensing growth, we think Playboy’s earnings are poised to grow rapidly. Analyst estimates from Capital IQ suggest EBITDA margins to jump from 10.4% in 2025 to 18.8% in 2027. This is likely to lead to doubling of EBITDA by 2027 (compared to 2025).

Peer Group Comparison

Risks

Tariff risk: The U.S.-China tariff tensions remain a key risk for the company. Any increase in tariff rates could impact Playboy’s supply chain and cost structure, leading to a decline in profitability, although we think Playboy can mitigate this with price increases and other strategies.

Geography risk: China accounts for a large portion of Playboy’s licensing revenue. Given the geopolitical tensions between the U.S. and China, rebuilding the China licensing business could be challenging.

Any macroeconomic slowdown could impact consumer spending and the demand for Playboy’s products.

Conclusion

Playboy’s shift toward a high-margin, asset-light licensing model is starting to yield tangible improvements in profitability, as evidenced by its return to positive adjusted EBITDA in Q1 2025, with more expected throughout 2025 and thereafter. With lower overheads, reduced debt burden, and long-term revenue visibility from licensing deals such as Byborg, Playboy is well positioned for sustainable growth. The continued turnaround of Honey Birdette, along with new category expansions and global licensing momentum, further enhances its earnings potential. Despite these structural improvements, Playboy’s current valuation does not fully reflect its long-term earnings potential, to say nothing of the franchise value for one of the world’s most iconic brands. As licensing continues to scale and margins expand, the company is poised for a meaningful re-rating.